I will be going to the MForesight Annual Summit on July 24-26, 2017 in Washington, DC. I serve on the Executive Committee and the Leadership Council for MForesight. It is a think-and-do tank focusing on the next generation technologies that will strengthen U.S. manufacturing. It is funded jointly by the National Institute for Standards and Technology (NIST) and the National Science Foundation (NSF).

As I think about the discussions that will take place at this upcoming event, I decided to summarize my thoughts, some relevant data and critical questions.

First some data. I will focus on US data although global data is clearly relevant and important.

Here is the total US manufacturing real output (from St Louis Fed):

Manufacturing output grew strongly till 2007, fell during the financial crisis and has rebounded since and is now nearly as high as it was at its peak.

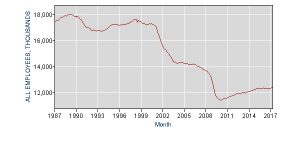

And here is the total number of people employed in manufacturing (from Bureau of Labor Statistics ):

While manufacturing as a fraction of total GDP has hovered in the range 11-13% over the last 50 years, the fraction of manufacturing employment over total employment has reduced from 24% to about 8%.

The loss of employment in the manufacturing sector has ben quite dramatic and is an issue of great importance and much debate. This can be attributed to two main factors: (1) increasing productivity per worker and (2) loss of jobs to other nations. There has been much recent research on both of these factors. First, here is the productivity from St Louis Fed:

BLS estimates that productivity growth in manufacturing was only 0.2% and 0.3% in 2015 and 2016 respectively. Bailey and Bosworth in the paper, “US Manufacturing: Understanding Its Past and Its Potential Future,” Journal of Economic Perspectives, have analyzed the outsized role played by computers and electronics sector in manufacturing output and productivity. They conclude, “In summary, the computer and electronics industry has a large impact on one’s evaluation of the performance of manufacturing. This part of the sector has had tremendous quality-adjusted output and productivity growth, even allowing for data errors. In contrast, the noncomputer part of manufacturing has exhibited very slow output and multifactor productivity gains and only moderate labor productivity growth.”

Loss of jobs has been analyzed in the economics literature. The most recent results along this line are in “Import Competition and the Great US Employment Sag of the 2000s” by Acemoglu et al in the Journal of Labor Economics, 2016. Quoting from their paper: “Between 2000 and 2007, the economy gave back the considerable employment gains achieved during the 1990s, with a historic contraction in manufacturing employment being a prime contributor to the slump. We estimate that import competition from China, which surged after 2000, was a major force behind both recent reductions in US manufacturing employment and—through input-output linkages and other general equilibrium channels— weak overall US job growth. Our central estimates suggest job losses from rising Chinese import competition over 1999–2011 in the range of 2.0–2.4 million.”

With this background, we may begin to ask some key questions for the future of manufacturing in the US:

- How can traditional manufacturing industries become more productive? Certainly, part of the answer depends on specific manufacturing sectors. Some candidate technologies include: cloud computing, sensors and controls, big data analytics, energy efficiency, etc. Better understanding of the potential of technologies by manufacturing sector will be crucial.

- What emerging technologies will have outsized impacts on the future of manufacturing? There are two ways to think about this. One is to consider impact on existing industries and products. This is addressed in question 1 but can be expanded to include emerging technologies such as nanotechnology, biotechnology, machine learning and artificial intelligence, etc. The other is to think about new product categories that do not yet exist but could be enabled by emerging technologies and become large industry sectors over time. Such new products could meet current needs in new and disruptive ways or meet new needs. We need to have better understanding of both these aspects.

- What new academic R&D efforts are needed to in view of the above analysis? Academic R&D ranges from long-term basic research to translational and applied research. From the US manufacturing point of view, we must take into account the key insights gained by the above analysis to shape the academic R&D agenda and develop productive public-private partnerships. Engineering Research Centers, Industry-University Cooperative Research Centers, Manufacturing Innovation Institutes are examples of current models of federally funded research activities. How can these be guided from the manufacturing perspective for maximum success?